Here’s a breakdown of the situation:

The Issue:

During a public hearing for Order 24-133, the Finance Director reportedly used a draft, not the final audited version, of the City’s Certified Annual Financial Report (CAFR) to calculate the unassigned fund balance.

Why is this a problem?

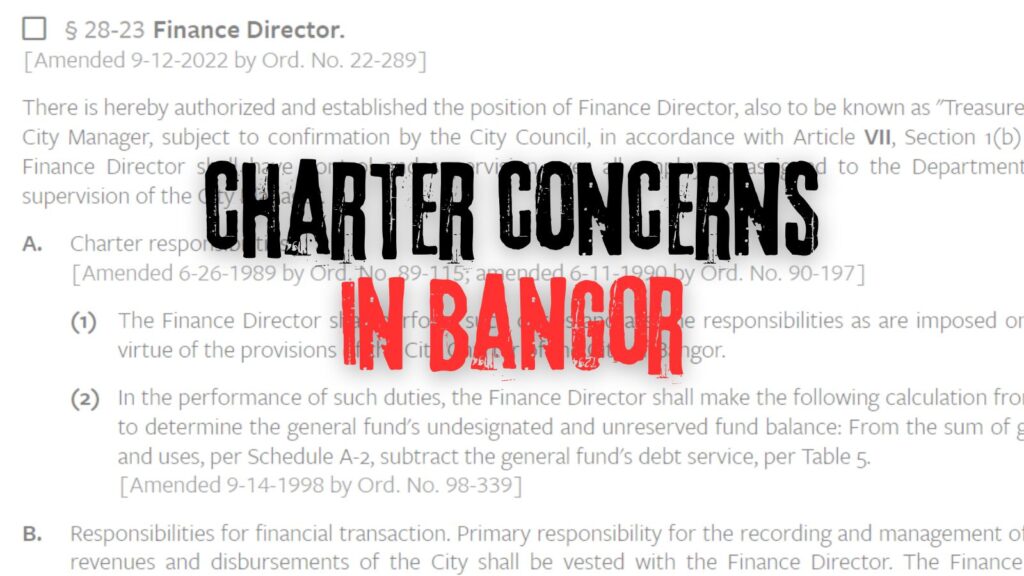

The City Charter, Section 28-23(A)(2), clearly mandates using the final, audited report for calculating the unassigned fund balance. This ensures financial information used for decision-making is accurate and reliable.

What are the concerns?

- Accuracy of Information: Relying on a draft report raises concerns about the accuracy of the information used by the Council for decision-making on Order 24-133.

- Transparency and Public Trust: Using a draft report undermines transparency and could cause confusion for the public. Order 24-133 itself references a completed audit that wasn’t finished at the time.

What is requested from the City Council?

- Correction of Public Record: Amending Order 24-133 to remove the reference to a completed audit for fiscal year 2023.

- Confirmation of Future Practices: Public confirmation that only final, audited reports will be used for calculating the unassigned fund balance, as mandated by the Charter.

Additional Considerations:

- Implementing an internal policy to clarify the use of the final audited report.

- Reviewing the decision-making process to prevent similar situations in the future.

- Amending §28-23(A)(2) to reflect the current name “unassigned fund balance.”

- Adding a due date for the City Manager’s annual report to ensure timely access to audited information for the Finance Director.

By taking these steps, the City Council can strengthen public trust and ensure adherence to the Charter for responsible financial management.

For further information:

You can access a copy of the City Charter here.

Copy of the email sent to Bangor City Councilors by Michael Beck

Dear City Council Members,

I am writing to request a review of a potential violation of the City Charter that arose during the City Council meeting held on April 22, 2024.

During the public hearing for Order 24-133 in that meeting, the Finance Director stated that a draft of the City’s Certified Annual Financial Report (CAFR) was used to calculate the unassigned balance used in an order voted on by the Council that same evening. (Youtube Video Link)

The Director expressed confidence in the draft numbers and indicated past audits haven’t resulted in significant changes. While these assurances are appreciated, the core issue lies with adherence to the City Charter.

Section 28-23(A)(2) of the Charter explicitly states:

In the performance of such duties, the Finance Director shall make the following calculation from the annual audit report to determine the general fund’s undesignated and unreserved* fund balance: From the sum of general fund expenditures and uses, per Schedule A-2, subtract the general fund’s debt service, per Table 5.

(*In 2012 the Charter was amended to change the name from “undesignated and unreserved” to “unassigned” fund balance. This ordinance was not updated to reflect the change in name.)

The Charter clearly mandates using the final, audited report – not a draft CAFR – for calculating the unassigned balance. This ensures the financial information used for decision-making is subject to the rigorous audit process, which can identify and correct potential errors.

Regardless of the potential accuracy of the draft information, the principle of adherence to the City Charter is paramount. Upholding these established processes fosters transparency, public trust, and ensures the Council has access to the most reliable financial data for crucial decision-making.

Order 24-133 contains a misstatement of fact.

Order 24-133 passed by the City Council references the ‘audit for fiscal year ending 2023’ in determining the unassigned fund balance. However, the Finance Director previously stated that evening the audit for fiscal year 2023 was not completed. This discrepancy may cause confusion for the public.

The statement in question: “The audit for fiscal year ending 2023 indicates that the City has an unassigned fund balance of approximately $19.9 million which represents 16.84% of the prior year expenditures.”

Desired Outcomes

To ensure public trust and adherence to the City Charter, I urge the City Council to consider the following:

Correction of Public Record: An amendment to Order 24-133 to remove the reference to a completed audit for fiscal year 2023. This ensures the public has access to accurate information.

Confirmation of Future Practices: Confirmation that the final, audited report will be used for all future calculations of the unassigned fund balance, as mandated by the Charter.

Corrective Measures for Consideration

Short-Term: Implementation of a new internal policy that clarifies the use of the final, audited report for calculating the unassigned fund balance.

Long-Term: Amend Section 28-23(A)(2) of the City Charter to reflect the current name “unassigned fund balance.”

Improved Processes

Investigation and Review: A thorough investigation and review of this situation is necessary. This review could examine the decision-making process that led to using the draft report, as well as potential improvements to internal controls to ensure adherence to the Charter in the future. The City Council may also consider a referral to the City’s Board of Ethics, depending on the findings of the internal review.

Add a Due Date for the Annual Report: Amend Section 28-21(D) to include a specific due date for the City Manager’s annual report. For example: “no later than December 31st of the same calendar year in which the fiscal year ends.” This can ensure the Finance Director has timely access to the final, audited information.

By taking these steps, the City Council can strengthen public trust, ensure adherence to the Charter, and implement best practices for future financial reporting.

Thank you for reviewing my concern. I am confident that the City Council will take the necessary steps to ensure adherence to the City Charter.

Respectfully,

Michael Beck